The smell of wet asphalt mixes with the sharp, clean scent of protective plastic clinging to the seats of a brand-new Chevrolet Blazer EV. Outside the showroom glass, heavy clouds hang low over a quiet row of electric SUVs. You grip a printout of the federal tax guidelines, your thumb tracing the ink where it outlines the strict new battery sourcing rules. The math on the window sticker no longer seems to work in your favor, leaving you with the quiet frustration of a missed opportunity.

Inside the dealership lobby, the low hum of a printer is interrupted by the soft clink of a ceramic coffee mug. Sales representatives speak in hushed tones, offering glossy brochures that boast about electric range while carefully bypassing the immediate financial reality. This sudden sticker shock can make you feel like you are arriving at a party just as the music stops.

Yet, behind the glass doors of the finance office, a different conversation is happening. Financial managers sit behind wide monitors, entering codes that quietly route around the very restrictions stalling showroom sales. They are not bending the rules; they are simply using a parallel highway that the federal government left wide open for those who know how to ask for it.

The Backdoor Bridge: Why the Front Gate Is Not Your Only Option

To understand how this works, you have to stop looking at the electric vehicle tax incentive as a single, rigid wall. Instead, think of it as a house with a locked front door and a wide-open side gate designed for commercial deliveries. The front door is Section 30D of the tax code—the consumer credit. It is fussy, demanding, and highly sensitive to where General Motors sources its battery minerals and components. When GM lost its eligibility for certain models due to these strict sourcing rules, the front door locked for everyday buyers.

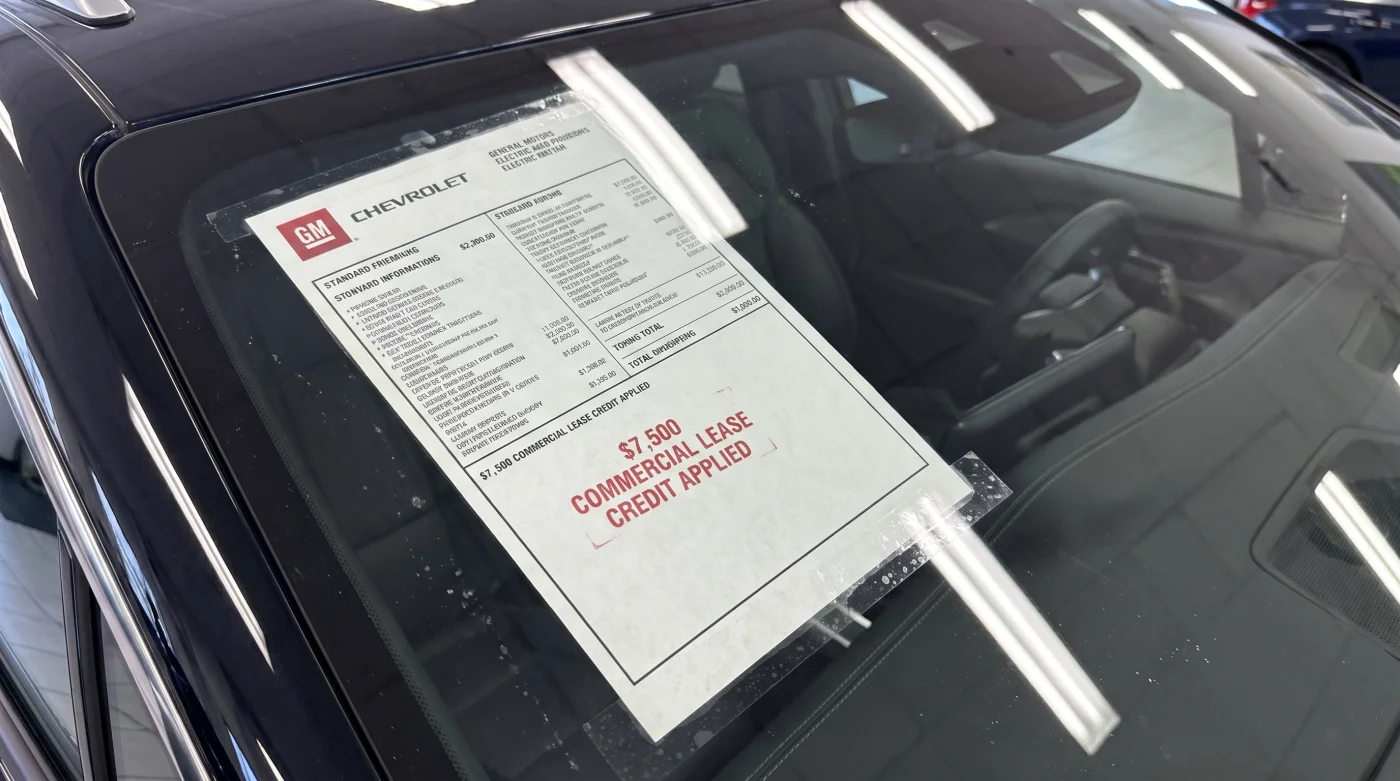

However, the side gate is Section 45W, which governs commercial vehicle credits. The federal government treats leased vehicles as commercial property because they are owned by the financial institution, not you. Because of this classification, the strict battery assembly and mineral sourcing rules that disqualify General Motors vehicles from the consumer credit simply do not apply. The leasing company receives the full seventy-five hundred dollar credit instantly, and they can choose to pass those savings directly to you in the form of a capitalized cost reduction.

- California DMV network outage exposes critical flaw in digital title registration

- Ferrari Luce electric architecture abandons traditional lithium for high frequency capacitors

- Tesla Model 3 suspension geometry fails when compared against budget Chevrolet platforms

- Tesla Model Y owners report aggressive battery degradation from fast charging

- Toyota Tundra recall triggers massive dealership inventory gluts as loyal buyers suddenly vanish

A Whisper from the Finance Office

Marcus Vance, a forty-eight-year-old independent auto broker from Chicago, spent years watching buyers walk away from brilliant machinery over paperwork details. When the updated tax rules hit General Motors hard, he stopped focusing on traditional purchases entirely. He began structuring leases that utilized the commercial loophole, turning disappointed shoppers back into owners. He calls it the only clean transaction left in the electric vehicle market, a quiet adjustment that levels the playing field for the average driver.

Matching the Loophole to Your Driving Style

For the Daily Commuter

If your daily drive consists of short trips to the office and weekend errands, leasing is already a natural fit. By applying the commercial credit to a lease on a Lyriq or an Equinox EV, you offset the depreciation that occurs during the first three years of ownership.

This strategy allows you to experience the refined, quiet cabin of a modern electric vehicle without worrying about long-term battery degradation. You secure low monthly payments while keeping your hard-earned capital in your bank account, rather than tying it up in an asset that is rapidly evolving.

For the Long-Term Owner

You might prefer to own your vehicles for a decade, making a lease seem counterintuitive at first glance. However, the commercial lease workaround can be used as a temporary bridge to full ownership.

You can structure a short-term lease to capture the seventy-five hundred dollar discount upfront, and then buy out the lease after a few months. This simple two-step maneuver bypasses the strict federal purchase penalties, delivering the vehicle into your garage with the discount fully intact.

The Clean Escape: How to Execute the Lease Workaround

Executing this strategy requires a quiet confidence when you sit down at the negotiating table. You do not need to argue; you simply need to request the correct structure.

Ask the dealer directly if they are passing the Section 45W commercial credit through as a capitalized cost reduction on the lease. Most major manufacturer captive lenders do this automatically to move inventory, but verifying the line item on the lease worksheet is vital.

- Confirm that the seventy-five hundred dollars is listed as a capitalized cost reduction, not a dealer discount.

- Check the acquisition fee and the money factor to ensure the dealer is not clawing back the savings through inflated interest rates.

- Verify the lease buyout terms to ensure there are no early payoff penalties if you plan to purchase the vehicle immediately.

Use this tactical toolkit to keep the transaction transparent and clean:

| Lease Term to Watch | Target Value / Action | Value to You |

|---|---|---|

| Capitalized Cost Reduction | Full $7,500 applied immediately | Lowers your monthly payments or buyout price |

| Money Factor | Compare to current prime lending rates | Prevents the dealer from hiding extra fees in the interest |

| Early Buyout Clause | No penalty after 30 to 90 days | Allows you to transition to full ownership cheaply |

Reclaiming the Financial High Ground

Navigating the transition to electric mobility should not feel like trying to solve a puzzle in the dark. When federal regulations change, the market naturally adapts, finding new pathways to keep vehicles moving and prices reasonable. Understanding these structural shifts puts the control back where it belongs—in your hands.

By looking at the transaction through the lens of a commercial lease, you strip away the confusion and frustration of the showroom floor. You get to drive away in a highly capable vehicle, comfortable in the knowledge that you outsmarted the system simply by paying attention to the fine print.

“The smartest buyers don’t try to change the rules of the game; they simply learn how the rules are organized behind the scenes.”

Frequently Asked Questions

Does my personal income level disqualify me from using this lease loophole?

No. Unlike the consumer tax credit, the Section 45W commercial lease credit has no household income limits or caps.</pCan I buy out the lease immediately to own the GM vehicle permanently?

Yes, most GM Financial leases allow you to buy out the lease within the first few months without penalty, securing the discount.</pDo I have to claim this credit on my annual tax return?

No, the leasing company claims the credit and applies it directly to the vehicle deal, meaning you do not have to wait until tax season.</pAre all General Motors electric vehicles eligible for this lease workaround?

Yes, any electric vehicle leased through a participating financial institution can qualify for the Section 45W commercial credit.</pWill I need to pay a high interest rate on a lease compared to a purchase loan?

It depends on current tier promotional rates, but you should always compare the money factor to ensure the tax savings aren’t eaten up by finance charges.