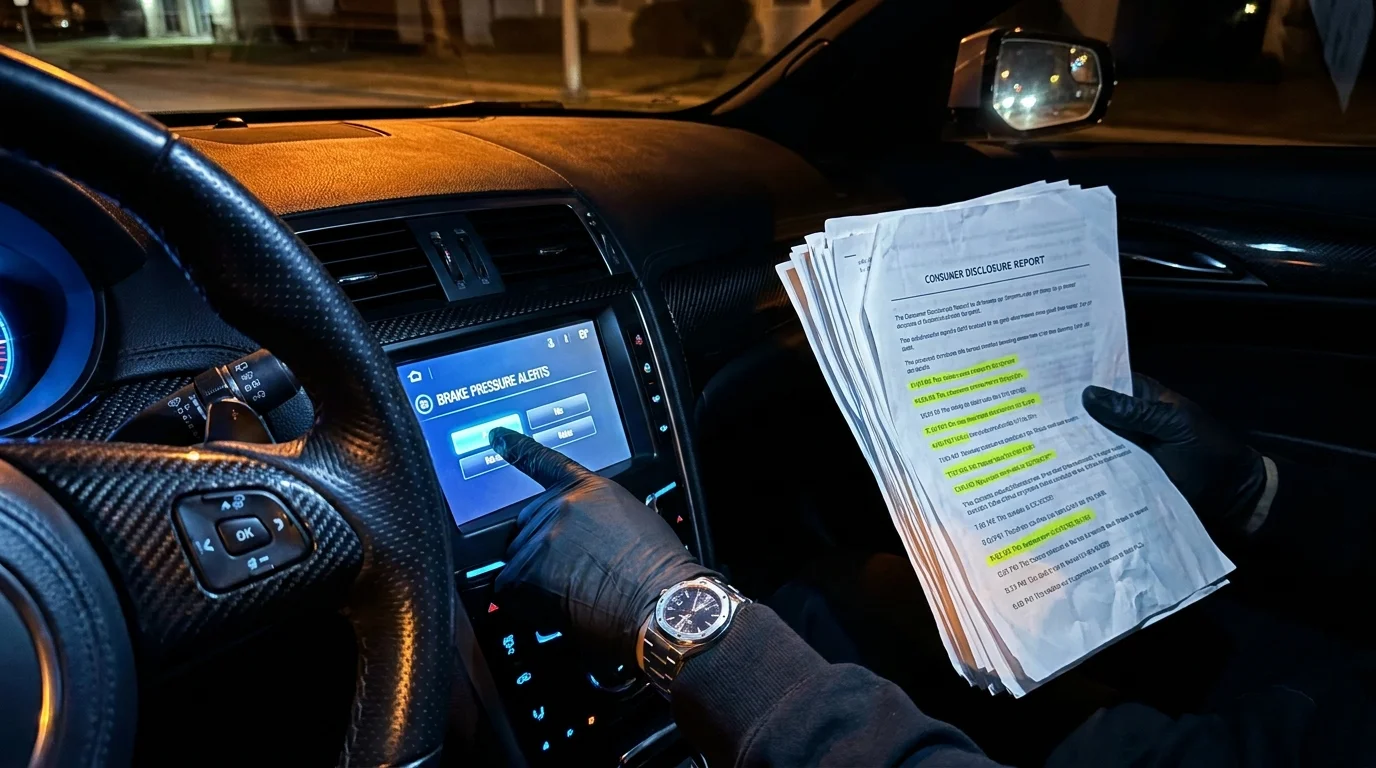

The morning light filters through the kitchen window, catching the fine dust motes settling on a thick, double-sided document. It is a fifty-page consumer disclosure report, fresh from the envelope, smelling faintly of commercial ink and warm paper. Across the middle of page thirty-seven, a yellow highlighter marks a series of raw numbers: a sequence of decimal points indicating brake pedal pressure, registered at eighty-three percent on a rainy Tuesday morning. You remember that moment vividly—a sudden, heart-stopping stop when a delivery truck cut you off, but to the machine reading this page, it is simply a black mark of high-risk behavior.

For decades, we believed that a clean driving record was an unshakeable shield. If you avoided accidents, paid your tickets, and kept your vehicle maintained, your insurance company rewarded you with stable, predictable premiums. Today, that silent agreement is broken, replaced by an invisible ecosystem of connected car telemetry where every stoplight, curve, and emergency maneuver is packaged, priced, and sold without your explicit knowledge, destroying the assumption that a clean driving record guarantees your low rates.

The reality is that your modern vehicle is no longer just a mechanical tool of transportation; it has become a rolling data harvester. We treat our vehicles as private sanctuaries, but they behave like data-harvesting smartphones on wheels, quietly logging every physical action you take behind the wheel.

The Passenger in the Dashboard

To understand how this system operates, we must look past the sleek marketing of modern vehicle connectivity. When you sign the paperwork for a new car or update its companion mobile application, hidden deep within the dense, thirty-page terms of service is a small clause granting the manufacturer permission to share your driving telemetry. This data does not stay with the carmaker; it is fed directly into massive repositories run by firms like LexisNexis Risk Solutions and Verisk. Behind the dashboard glass, complex cellular modems stream your physical habits directly to third-party data brokers who compile risk profiles designed to maximize insurance company profits.

These corporations compile what they call consumer safety profiles, which act as a secret credit score for your driving habits. A single hard brake, often defined as a deceleration of more than eight miles per hour within a single second, is flagged as a high-risk event, regardless of whether you were avoiding an accident or simply slowing down for a yellow light. The software lacks human context; it only sees the sudden drop in speed and registers you as an aggressive driver, silently doubling your premium upon renewal.

Marcus Vance, a forty-two-year-old high school physics teacher from Columbus, Ohio, spent years maintaining a spotless record, only to find his monthly premium increase by one hundred and forty dollars. When Marcus requested his personal LexisNexis file, he discovered over two hundred recorded instances of hard braking and rapid acceleration—almost all of which occurred during his daily commute through a highly congested school zone where stop-and-go driving was a physical necessity for safety. He was flagged as a dangerous driver for a single hard brake that actually saved a pedestrian.

- ClearMotion suspension algorithms forcefully push cabin floors against pavement undulations

- Polestar factory leaks expose a rigid aerospace aluminum chassis bonding process

- Ford BlueCruise highway steering entirely disables when drivers wear polarized pilot sunglasses

- Kia EV9 buyers face a shocking yearly registration penalty ignoring state weight fees

- Lucid Air cabin silence embarrasses budget electric cars through thick laminated acoustic flooring

The Telemetry Trap Across Different Vehicles

The impact of this silent surveillance varies significantly depending on what you drive and how your vehicle connects to the cellular network. The system does not treat all drivers equally, and certain vehicle types carry higher inherent risks of background data exposure.

For the highway commuter, the primary threat lies in adaptive cruise control systems that react sharply to merging traffic. These systems often trigger automated braking events that the car logs as manual driver panic, automatically updating your risk profile with false indicators of erratic behavior. Your vehicle companion app may be quietly selling this data under the guise of driver reward programs that promise discounts but actually harvest raw behavioral metrics.

Urban electric vehicle owners face an entirely different set of challenges due to regenerative braking systems. When you lift your foot off the accelerator, the electric motor reverses to capture energy, creating a rapid deceleration curve that some older telemetry algorithms mistakenly classify as hard physical braking. This systemic misinterpretation means EV drivers are often unfairly penalized simply for utilizing their vehicle’s standard efficiency features.

Reclaiming Your Digital Footprint: The Step-by-Step Opt-Out

Stopping this flow of private telemetry requires a methodical, deliberate approach to your digital vehicle settings and your rights under consumer protection laws. You do not have to accept this silent surveillance as an inevitable cost of modern vehicle ownership. Taking control of this data is the single most effective way to protect your budget from unpredictable premium spikes.

To cut off the flow of your personal driving data to insurers, follow these specific technical steps to clean up your profile and revoke data sharing permissions:

- Request Your Consumer Disclosure Report: Visit the LexisNexis Risk Solutions consumer portal online and submit a formal request for your Full File Disclosure. This report is legally free under the Fair Credit Reporting Act and will show you exactly what telemetry has been collected.

- Submit a Verisk Consumer Inquiry: Follow the same process with Verisk, the second major data broker in the automotive space, to review and challenge any inaccurate driving events recorded under your vehicle identification number.

- Revoke Telemetry Sharing in Your Vehicle App: Open your car’s mobile application, navigate to the privacy settings or account profile, and locate terms like Smart Driver, Drivewise, or Connection Services. Toggle these options completely off to stop the real-time upload of pedal telemetry.

- Contact Your Automaker Directly: If the mobile app options are unclear, call your manufacturer’s customer relationship center and request a complete opt-out of third-party data sharing for your specific VIN.

By executing these steps, you build a digital firewall between your vehicle’s onboard computer and the financial institutions that use your daily habits to adjust your rates. Taking charge of these portals represents your ultimate defense against digital overreach.

Restoring the Sanctuary of the Road

Ultimately, driving should be an experience of focus, safety, and personal peace of mind. When every movement of your foot is monitored and monetized, the simple act of navigating daily traffic becomes a source of quiet anxiety, forcing you to choose between natural defensive driving and the fear of a digital penalty.

By reclaiming authority over your personal telemetry, you preserve the traditional boundaries between your private life and corporate balance sheets. Protecting your digital footprint ensures you can go back to reclaiming your personal telemetry and driving with absolute confidence, free from the shadow of background data brokers.

Your driving habits belong to you, not to the balance sheets of data brokers looking to monetize a split-second defensive maneuver.

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| Data Broker Harvesting | LexisNexis and Verisk compile secret driving scores from connected vehicle telemetry. | Explains why clean records no longer guarantee low insurance premiums. |

| Hard Braking Metrics | Deceleration of over 8 mph in one second triggers automatic high-risk flags. | Provides the precise technical threshold that causes hidden premium increases. |

| Opt-Out Rights | The Fair Credit Reporting Act allows you to view and freeze your driver profile. | Gives you the legal leverage to stop automakers from selling your pedal telemetry. |

Frequently Asked Questions

How do I know if my car is actively sending my driving data to LexisNexis?

You can confirm this by requesting your free consumer disclosure report directly from the LexisNexis portal, which will list every timestamped event recorded from your vehicle.Can my insurance company drop my coverage based solely on this telemetry data?

While they rarely cancel policies outright, they use this data to aggressively adjust premium rates or deny standard renewal discounts upon policy expiration.Will opting out of data sharing disable my car’s navigation or safety features?

No, opting out only stops the external transmission of your driving data to marketing brokers; your vehicle’s physical safety features will continue to function normally.How long do hard braking events remain on my data broker profile?

Under federal consumer reporting guidelines, these behavioral records typically influence your risk score for up to three to five years from the date of capture.Are all modern car manufacturers participating in these data broker networks?

Most major brands have partnerships with data brokers, but the specific models and opt-out methods vary depending on your vehicle’s cellular package.