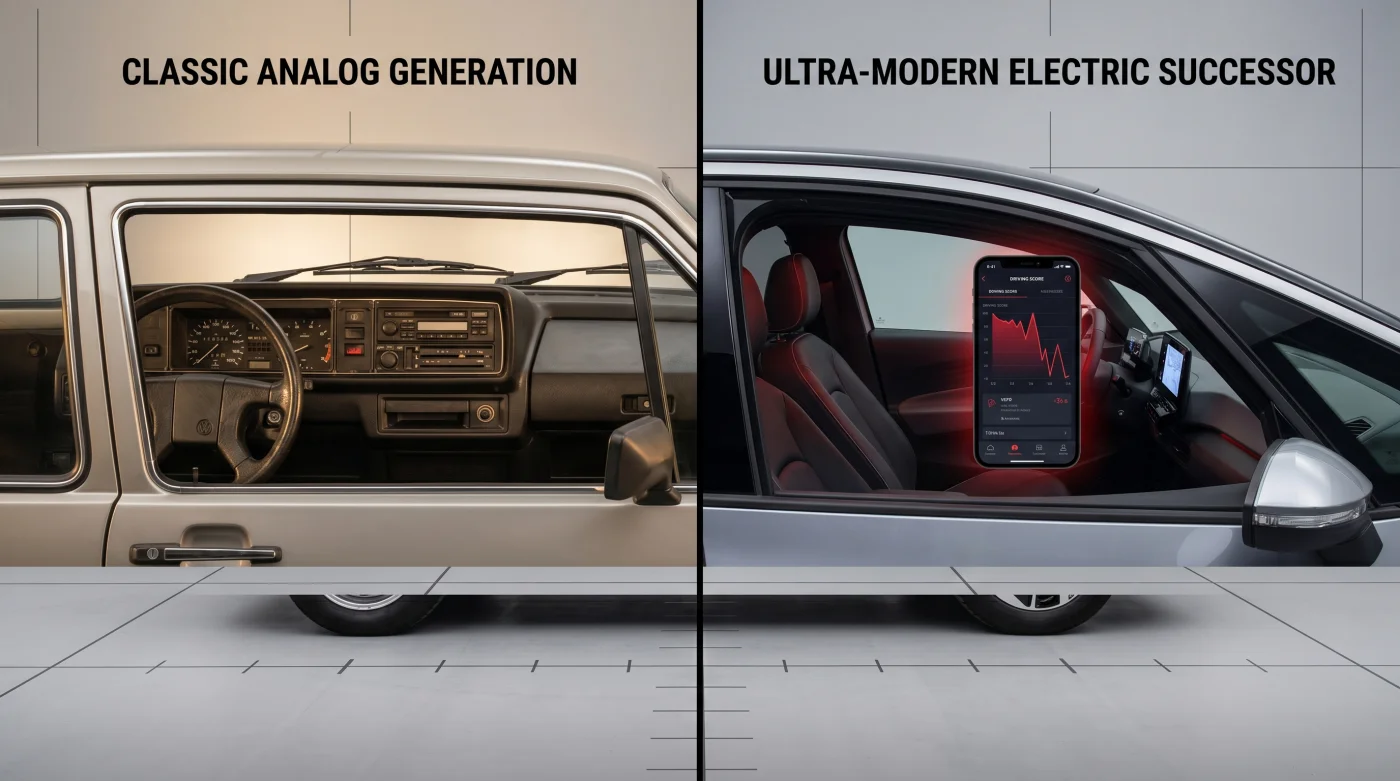

The cold blue glow of your smartphone illuminates the dashboard of your sedan as you navigate a damp, slick arterial road at twilight. The heater vents hum softly, blowing dry air against the windshield to fight the creeping fog. Under your tires, the wet asphalt hums a steady, rhythmic song. Everything feels controlled, predictable, and quiet, until a delivery van suddenly blows through a clear red light directly in your path.

Your survival instincts take over in a millisecond. Your foot plunges into the floorboard, engaging the anti-lock brakes with a violent, rhythmic pulsing beneath your sole. Your seatbelt bites hard into your shoulder as the car halts inches from the van’s sliding door. Your heart hammers against your ribs, but you are safe, uninjured, and your car is intact. Yet, a soft chime from your dashboard mount breaks the silence, announcing that your digital score has just suffered a sharp drop in velocity instead of celebrating your perfect defensive reflex.

This is the hidden cost of smartphone insurance telematics, a system rapidly adopted by millions of young drivers looking to escape skyrocketing premium costs. These apps monitor your daily habits under the promise of personalized discounts based on how safely you drive. In reality, the algorithms operating behind the screen are blind to the chaotic environment beyond your windshield, translating your most critical defensive maneuvers into financial penalties.

The Mirage of the Algorithmic Discount

Insurance companies pitch telematics as a win-win partnership. By downloading an app that tracks your speed, acceleration, cornering, and braking, you theoretically prove your low-risk status and earn lower monthly bills. The logic sounds fair on paper: drive like a responsible citizen, pay less than the speed demons. However, this system relies on a flawed assumption that all rapid deceleration is a sign of reckless, distracted driving, creating a deeply flawed monitoring environment for everyone involved.

By converting your phone’s internal micro-electro-mechanical systems (MEMS) accelerometer into an automated judge, the system betrays its own promise of fair assessment. The algorithm cannot see the stray dog, the distracted pedestrian stepping off the curb, or the red-light runner you just avoided. It only sees a sudden, steep drop in speed over a fraction of a second, immediately logging a black mark against your profile.

- Mazda MX-30 rotary range extenders intentionally consume motor oil to lubricate internal seals

- 2027 Nissan Z redesign details leak a mandatory dual-clutch transmission replacing the manual

- NACS charging adapters trigger severe thermal throttling on legacy 400-volt electric vehicle architectures

- Tesla Full Self-Driving abruptly brakes when digital billboards mimic emergency vehicle strobe frequencies

- Hyundai Ioniq 5 lease contracts hide a commercial tax loophole dealerships actively suppress

For young drivers under twenty-five, who face some of the most punishing insurance rates in the country, this algorithmic blind spot creates a highly stressful dilemma. They are forced to choose between defensive maneuvers that prevent real-world sheet metal damage and maintaining a pristine digital profile to keep their weekly budget afloat.

The 0.6g Threshold: Marcus Vance’s Costly Reflex

Consider the experience of Marcus Vance, a twenty-three-year-old nursing assistant from Columbus, Ohio. Marcus installed his insurer’s tracking app to trim forty dollars off his steep monthly premium. For three months, he drove with meticulous care, keeping his phone locked firmly in a heavy-duty dashboard cradle. His score hovered at a near-perfect ninety-eight percent, promising a significant discount at his upcoming policy renewal.

One rainy evening, a deer leaped from the shadows of a suburban road directly into his headlight beams. Marcus checked his rearview mirror, saw no trailing headlights, and applied firm, steady pressure to his brakes to avoid hitting the animal. He stopped safely, the deer bounded into the woods, and Marcus continued home. The next morning, his app notified him of a severe braking event, dropping his monthly score by twelve points and triggering a surcharge on his next renewal instead of the promised discount.

The app’s built-in accelerometer registered a deceleration force exceeding 0.5g, a typical threshold for many insurance algorithms to trigger an infraction. To the software, Marcus’s life-saving reflex was indistinguishable from a driver texting at fifty miles per hour and slamming the brakes at the last second. The algorithm’s lack of external cameras or radar data means it operates in a vacuum of context.

Navigating Different Roads: The Dual-Scoring Dilemma

The unfairness of telematics scoring varies wildly depending on your geography and daily driving routes. Drivers in dense urban centers face an entirely different set of environmental challenges than those navigating empty suburban avenues or rural highways, making the standard algorithmic calculations completely unfair for city commuters.

In heavy city traffic, aggressive lane-cutters and sudden yellow-light cycles are daily occurrences. If you brake firmly to avoid running a red light, the telematics app penalizes your score. If you slide through the intersection to keep your score intact, you risk a camera ticket or a broadside collision. This dynamic forces a dangerous choice between physical safety and financial punishment, disproportionately affecting city dwellers.

Rural drivers face their own set of algorithmic traps. Unpaved gravel roads, deep potholes, and sudden changes in pavement quality can cause the phone to shake violently within its mount. To a basic accelerometer, this sudden vibration looks identical to rapid swerving or erratic braking, turning a simple gravel driveway into a costly safety violation.

Defending Your Score: The Driver’s Tactical Guide

While you cannot rewrite your insurance company’s proprietary algorithm, you can take practical steps to minimize false positives. Managing how your phone experiences physical motion inside your cabin can prevent the software from misinterpreting normal road feedback as aggressive habits.

By applying a few tactical dashboard adjustments and changing your approach to traffic flow, you can protect both your physical safety and your financial score from automated errors.

Implementing these small adjustments changes the way your phone interacts with the vehicle’s cabin, shielding your telematics profile from standard road noise:

- Use a Rigid Vent Mount: Never leave your phone in a cup holder, passenger seat, or loose pocket. A sliding phone multiplies perceived g-forces during normal stops, registering as a severe braking event. Use a heavy-duty, screw-tight vent clamp.

- Double Your Following Distance: Maintain a four-second gap behind lead vehicles. This extra space gives you the luxury of gradual deceleration, keeping your braking forces well below the dreaded 0.6g threshold.

- Anticipate the Stale Green: When approaching an intersection where the pedestrian signal is already flashing red, lift your foot off the gas early and coast. Algorithms favor long, low-g decelerations.

The High Cost of Invisible Math

As insurance companies push deeper into automated risk assessment, the line between helpful technology and unfair surveillance continues to blur. Drivers are left navigating their daily commutes while walking an invisible tightrope, constantly second-guessing their safety instincts to appease a piece of code.

When you are forced to choose between dodging a collision and preserving your monthly budget, the system has failed its primary goal of promoting public safety. The road requires your full, unfragmented attention, not a lingering fear of how your next defensive maneuver will translate onto a server halfway across the country.

The ultimate irony of these apps is revealed at the end of every billing cycle. You can drive for weeks with flawless anticipation, only for a single, life-saving stop to erase your hard-earned progress, leaving you staring at a sharp, red downward spike on your digital driving score graph.

Read More