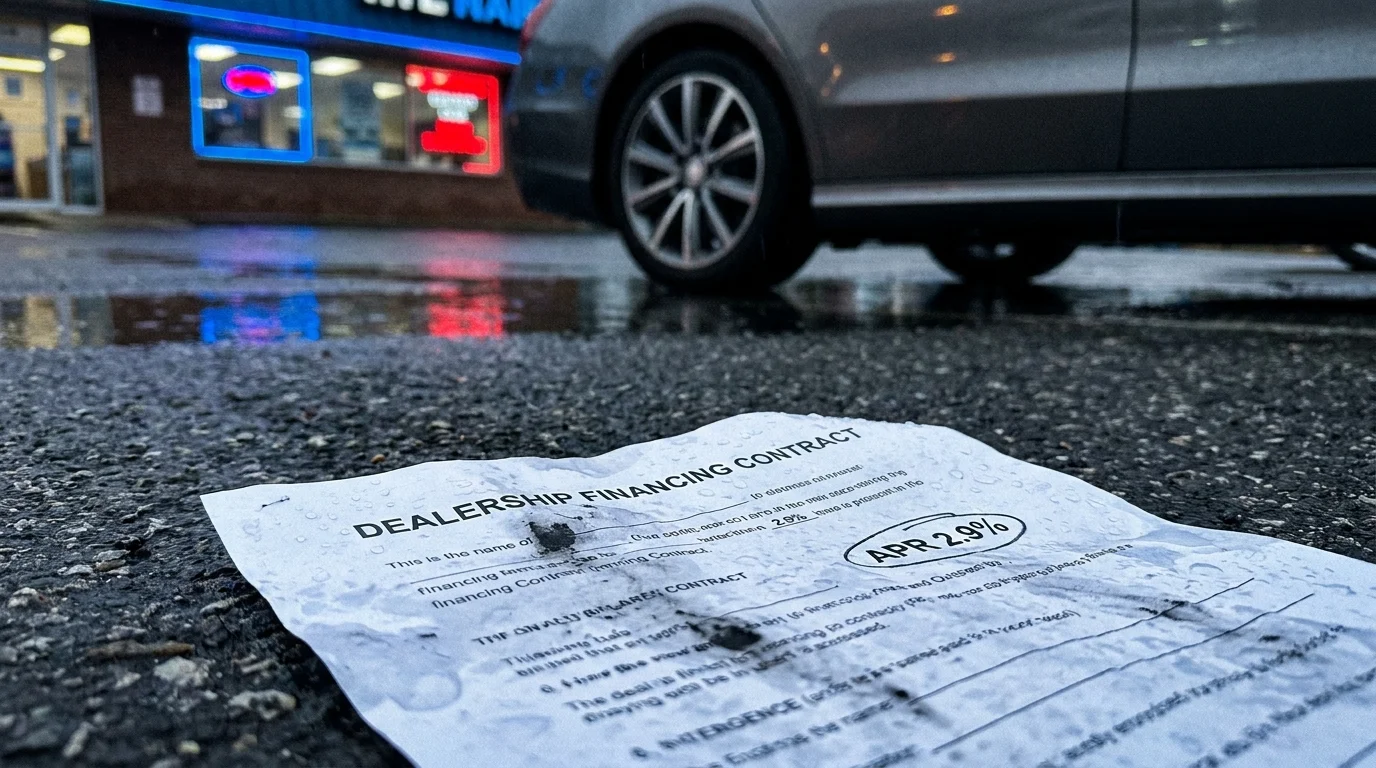

The low hum of the office laser printer is the only sound breaking the silence of the finance office. A stack of crisp, thirty-page contract sheets slides across the faux-mahogany desk, still warm from the toner. You look at the top line, feeling a quiet sense of victory because your phone screen shows a green checkmark next to a ‘Great Price’ certificate. You believe you bypassed the exhausting theater of car negotiations by using a trusted digital broker.

But as the finance manager hands you a heavy metal pen, the atmosphere in the room subtly shifts. **The actual paper contract** sitting before you contains numbers that do not quite match the triumphant spirit of your digital certificate. The monthly payment is forty dollars higher than your mental math predicted, wrapped in a web of terms that look official but feel incredibly heavy.

The truth is, the digital screen did not save you from the dealership trap; it simply escorted you directly to it. By relying on third-party algorithms to secure a low vehicle price, you unwittingly agreed to a sophisticated system designed to claw back every single dollar of that discount before you ever drive off the lot.

The Illusion of the Digital Shield

For years, car buyers have treated digital pricing apps as protective shields. We believe that if an algorithm analyzes local market data and stamps a price as ‘fair,’ the human element of deception is eliminated. This is the central logic flaw of modern car buying: assuming a digital middleman prioritizes your wallet over their own business model.

These platforms do not operate as public charities. **They are lead-generation machines** that sell your high-intent buying behavior to hungry dealership networks. When a dealer agrees to sell a car for a thin margin through an app, they are not taking a loss out of the goodness of their hearts. They are paying a hefty backend referral fee to the digital broker—often between $300 and $450 per vehicle sold.

To survive this model, dealerships treat the digital price as a loss leader. The algorithm-approved price is merely a hook to get your physical signature into the finance and insurance office, where the real profit extraction occurs through inflated loan terms, markup rates, and highly padded product packages.

- Used Subaru Outback inspections demand checking this specific suspension bushing bracket

- Ford Bronco Raptor dealer markups completely collapse forcing sudden inventory discounts

- Toyota RAV4 Prime thermal architecture heavily outclasses full electric winter commuting

- Genesis G80 used pricing exposes a massive flagship luxury discount reality

- Subaru Outback Onyx Edition hides the exact heavy transmission cooler Wilderness owners demand

The Inside Secret: The Dealer Reserve

Marcus Vance, a forty-two-year-old former finance director who spent nearly two decades inside high-volume auto groups in Atlanta, knows exactly how this pivot works. ‘When a customer walked in with a digital certificate, we didn’t sweat the low price,’ Marcus admits with a quiet shrug. ‘We actually celebrated. We knew that buyer was relaxed, their guard was down, and they believed the hard part was over. That made them incredibly easy to guide into a seventy-two-month finance plan loaded with marked-up interest rates.’

Marcus explains that dealerships routinely practice what is known as ‘interest rate padding’ or the ‘dealer reserve.’ If a bank approves you for a 5% interest rate, the dealership is legally permitted in most states to present you with a contract at 7%. **That hidden 2% difference** is pure profit, split between the lender and the dealership, which completely erases any upfront savings the pricing algorithm promised you.

How the Algorithm Targets Your Specific Profile

The system does not treat every buyer the same way. The financing algorithm categorizes your behavior to maximize profits based on how you approach the purchase.

The Monthly Payment Seeker: If you focus primarily on what you pay each month, the dealership will stretch your loan terms out to 72 or 84 months. This keeps your payment matching your digital quote while burying thousands of dollars in extra interest charges deep inside the contract.

The Pre-Approved Buyer: Even if you arrive with a loan from your personal credit union, the finance manager will use ‘captive finance matching.’ **They will leverage dealer-specific incentives** to pressure you into switching to their preferred lender, claiming it is the only way to honor the algorithm’s vehicle price.

The Cash Buyer: If you attempt to bypass financing entirely, you may find the dealership suddenly adding mysterious ‘dealer prep’ fees or claiming the vehicle you reserved is no longer available. Without the backend finance kickback, the thin margin of the digital price is no longer profitable for them.

Dismantling the Contract: A Step-by-Step Guide

To survive the finance office, you must abandon the belief that your digital certificate protects you. You must become your own advocate the moment the physical contract is printed. Follow these tactical steps to protect your money:

- Demand the ‘Dealers Buy Rate Sheet’: Ask to see the actual lender approval document showing the lowest interest rate you qualified for, not just the pre-printed contract rate.

- Enforce the 2% Rule: Never accept a dealer finance rate that is more than 1% to 1.5% above your independent bank pre-approval.

- Decline ‘Tied-In’ Extras: If a finance manager claims a warranty or gap insurance is required to get a specific interest rate, walk out. This practice is highly illegal.

- Run Your Own Math: Use an independent loan calculator on your phone to verify that the principal, interest rate, and term exactly equal the final monthly payment on the page.

Keep your focus on the physical document in front of you. **Do not sign any page** until you have personally calculated the total cost of the loan over its entire lifespan, rather than just focusing on the monthly payment figure.

Reclaiming Your Peace of Mind

Stepping away from the digital illusion requires a shift in how we view convenience. The convenience of a pricing app is not designed to save you money; it is designed to make the initial step of car buying so painless that you do not notice the sting of the final step.

True leverage does not come from a colored pricing graph on a smartphone screen. It comes from your willingness to stand up, slide the warm paper contract back across the desk, and walk out of the dealership if the math does not make sense. When you realize that you control the pen, the power dynamics of the entire room shift back in your favor.

“The most expensive car discount you will ever get is the one that forces you to sign a dealer-markup finance contract.” — Marcus Vance

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| The Broker Fee Trap | Dealers pay $300-$450 per lead to digital pricing services. | Explains why dealers must recoup margins through backend financing markup. |

| The Dealer Reserve | Dealers can mark up lender interest rates by up to 2%. | Allows you to negotiate the APR directly instead of just accepting the printed offer. |

| Captive Finance Pressures | Dealers may refuse digital pricing unless you use their in-house lenders. | Gives you the warning signs to look for before transferring your loan pre-approval. |

Frequently Asked Questions

Is the price on my digital buying certificate guaranteed by law? No. Digital pricing certificates are marketing agreements, not binding legal contracts, and dealers can add fees or require in-house financing to honor them.

How do I know if the finance manager marked up my interest rate? Always secure a pre-approval from a local credit union before visiting the dealer. If the dealer’s rate is higher than your pre-approval, they have likely padded the rate.

Can a dealer legally force me to buy a warranty to get a loan? Absolutely not. This is a predatory practice known as ‘predatory lending’ or ‘coercive tying,’ and it violates federal lending laws.

Why do dealers dislike cash buyers who use pricing apps? Cash buyers eliminate the dealer’s opportunity to make money on interest markups, meaning the dealer makes almost zero profit on an algorithm-priced vehicle.

What is the safest way to use a car pricing app? Use the app solely to find market averages, but arrange your own financing and negotiate the final out-of-the-door price independently.