The early morning air in the Nebraska panhandle carries a bite that cuts through a flannel shirt like a dull blade. You sit in the cab of a grain truck, the steering wheel cold beneath your palms, watching the diesel exhaust plume into the gray light. On the passenger seat lies a renewal notice from your insurance carrier, a document that feels less like a bill and more like a heavy wool blanket soaking up water. The premium jump is enough to make you wonder if the harvest is even worth the fuel.

Standard commercial insurance is built on a logic of high-speed interstates and cross-country fatigue. To the bean-counters in a glass tower, your truck is no different from a sleeper cab running twenty hours a day through Chicago traffic. They see the weight, the axles, and the liability, but they miss the dirt roads and the 150-mile circles that define your life. The premium logic is broken for the American farmer, and most agents are too comfortable with the status quo to fix it.

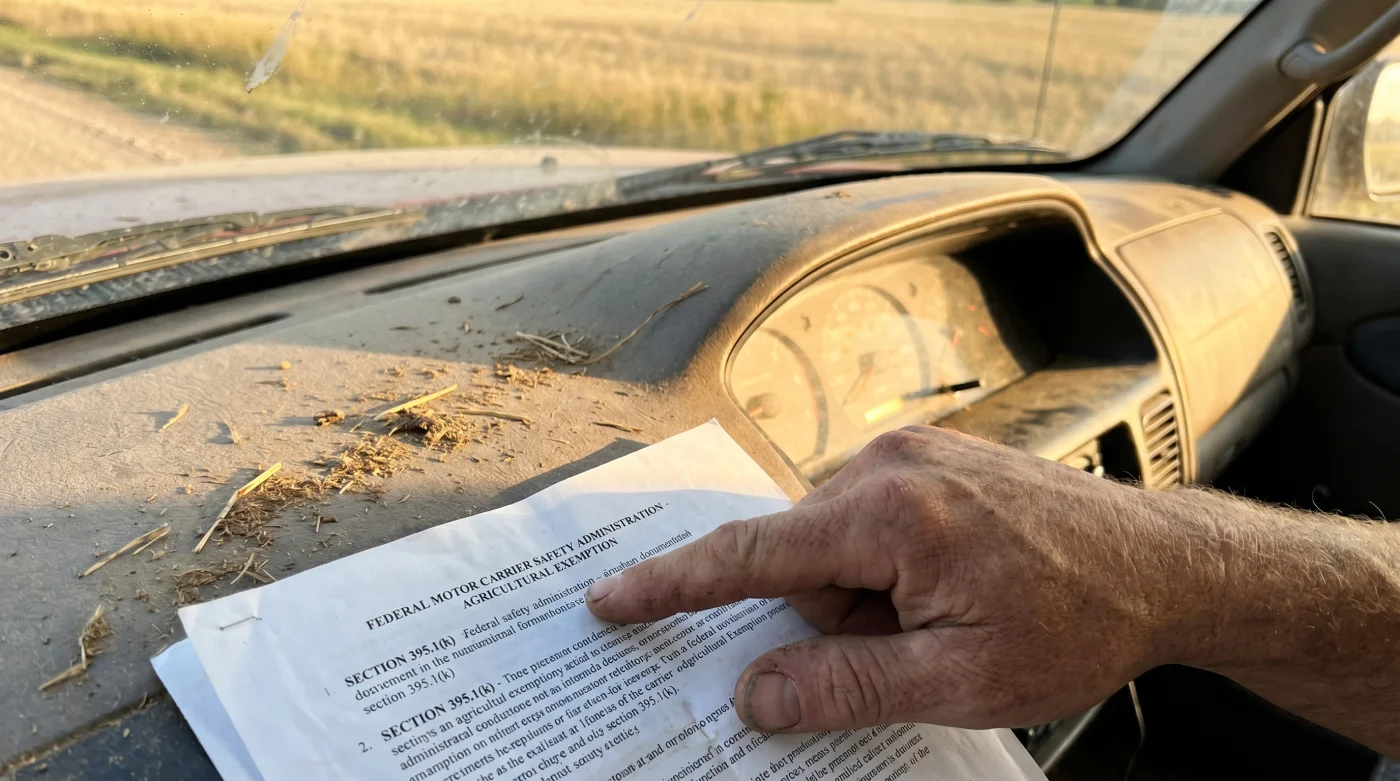

There is a silence in the industry regarding how the Federal Motor Carrier Safety Administration (FMCSA) actually views your operation. Most drivers assume that a heavy truck equals a commercial driver’s license (CDL), which in turn equals a commercial insurance rate that could choke a mule. But there is a shadow lane in the law, a specific exemption for Farm-Related Service Industries (FAS) that acts as a pressure release valve for your overhead.

The Ghost Lane of Federal Regulation

Insurance premiums are not a fixed mountain; they are a fluid system that reacts to how you are classified in the federal database. Think of the FMCSA regulations like a massive irrigation system. Most people are fighting to stay in the main canal where the current is strongest and most expensive. The FAS exemption is a side-gate that allows you to water your own fields without paying for the entire valley’s infrastructure.

- Ford patent filings reveal a roof-mounted backup battery charging system for stranded EVs

- Ford Bronco 2026 chassis leaks reveal an independent suspension ruining rock crawling capabilities

- GM vehicle safety recall 2026 exposes a critical battery monitoring software flaw

- Ford BlueCruise sensors aggressively disengage when encountering heavily shadowed mountain highway curves

- Ford Mustang Mach-E weight classification quietly bypasses strict heavy vehicle registration penalties

The perspective shift requires you to stop seeing your truck as a ‘commercial vehicle’ and start seeing it as ‘specialized agricultural equipment.’ When you stop following the standard long-haul playbook, you realize the system was never meant to be this rigid for us. It is about understanding the regulatory bypass that exists for those who keep their boots on the ground and their tires on the gravel.

Silas and the Twelve-Thousand Dollar Document

Silas Vance, a 59-year-old custom applicator out of Kearney, spent three decades paying premiums that assumed he was hauling hazardous materials through Times Square. During a particularly brutal renewal cycle last October, his agent quoted a 22% increase, citing ‘market volatility’ in the trucking sector. Silas didn’t get angry; he got specific. He spent an evening with a pot of black coffee and the FMCSA handbook, finding the FAS loophole that his agent had overlooked for twenty years.

By restructuring his filings to reflect the Farm-Related Service Industry exemption under 49 CFR Section 383.3, Silas proved his drivers didn’t need full-blown CDLs for their 150-mile radius. This single distinction allowed his insurer to reclassify his entire fleet. The resulting premium drop wasn’t a small discount; it was a $12,000 correction that felt like finding a buried cache of gold in the north pasture.

Adaptations for the Modern Producer

This isn’t a one-size-fits-all fix, but rather a set of adjustment layers that you must apply to your specific operation. The FMCSA has carved out these spaces because they know a farm truck isn’t a freight liner. You have to identify your specific niche to claim the savings that are already legally yours.

The Seasonal Specialist

For those whose trucks spend six months of the year tucked in a shed, the FAS exemption is a lifeline. You aren’t a year-round threat to the highway system, and your paperwork should reflect that. By utilizing restricted CDL provisions, you can bypass the ‘High-Risk Professional’ tag that insurers use to justify five-figure premiums.

The Livestock Movement Logic

Moving living cargo requires a different kind of focus, and the federal government recognizes the urgency of the haul. When you trigger the agricultural exemption for livestock, you are operating under a different risk profile. This isn’t just about hours-of-service; it’s about the insurance industry’s perception of your reliability and the necessity of your route.

Claiming the Section 383.3 Correction

The solution isn’t found in a new insurance company; it is found in the ‘Remarks’ section of your policy filing. You must be mindful and minimalist in your approach, ensuring every box checked aligns with the FAS criteria. Use this tactical toolkit for renewal to ensure you aren’t leaving money on the table.

- Identify 49 CFR Section 383.3(e) in your federal filing documents.

- Verify your operation stays within the 150-air-mile radius of the farm or farm-related business.

- Confirm your drivers are operating vehicles specifically for farm-related service industries like custom harvesters or farm retail outlets.

- Present the ‘Restricted CDL’ status to your underwriter as a primary risk-mitigation factor.

When you sit down with your agent, don’t ask for a discount. Instead, instruct them to audit the vehicle classification against the FAS criteria. The goal is to move your policy from the ‘Standard Commercial’ bucket to the ‘Ag-Exempt’ bucket. It is a quiet, administrative shift that carries the weight of a massive windfall.

Reframing the Cost of Doing Business

Mastering these regulatory details does more than just save a few thousand dollars; it restores a sense of agency in a market that often feels rigged. There is a specific kind of peace that comes from knowing you aren’t being overcharged for a risk you don’t represent. It allows you to breathe through the pillow of rising costs and focus on the actual work of the land.

Reflecting on these rules reminds us that the law, while often dense and frustrating, has pockets of common sense. Finding those pockets is the difference between a farm that thrives and one that merely survives. When the overhead pressure is relieved, you can invest back into the machinery, the soil, and the people who make the harvest possible. It is about reclaiming your margin from the bureaucracy.

“True savings in the agricultural sector are never found in the sales pitch, but in the fine print of federal exemptions.”

| Key Point | Regulatory Detail | Added Value for the Reader |

|---|---|---|

| FAS Exemption | 49 CFR 383.3(e) | Bypasses the need for full CDL premiums in ag sectors. |

| Operational Radius | 150-Air-Mile Limit | Categorizes the risk as local/low-impact versus interstate. |

| Policy Reclassification | Underwriter Audit | Forces the insurer to use lower-tier agricultural rate tables. |

Do I need a CDL if I qualify for the FAS exemption? No, the FAS allows for a restricted license or a complete waiver depending on state-level adoption of federal standards. Does this apply to hired hands or just family? It applies to employees of farm-related service industries, provided they meet the mileage and utility requirements. What is the ‘Magic Section’ for insurance agents? Explicitly mention 49 CFR Section 383.3 to trigger a re-evaluation of the driver’s risk profile. Will this affect my ability to haul across state lines? Yes, the 150-mile radius is the hard limit; crossing state lines is fine as long as you remain within that circle. How much can I realistically save? Many operators see a 15% to 30% reduction in premiums once the ‘Commercial’ tag is replaced with ‘Ag-Restricted’.