The rainy Tuesday evening air hangs heavy in the dealership lot, smelling of wet asphalt and fresh tire gloss. Under the bright showroom halogen lights sits a pristine family SUV, its window sticker boasting a bold, clean price tag. You look at that number and think you know the terms of the engagement. You have calculated your budget down to the dollar, confident that the price on the glass is the mountain you have to climb.

Behind the frosted glass door of the Finance and Insurance office, the atmosphere changes. The air is cooler here, smelling of expensive cologne and heated laser printer paper. Dual monitors glow softly, casting a blue light over a desk where a heavy chrome pen rests on a stack of carbon-copy contracts. **The real transaction happens here**, silent and completely invisible to the casual buyer waiting on the vinyl couch outside.

You are tired after three hours of trading paint over the value of your old trade-in and negotiating the cost of the floor mats. When the finance manager slides the final paperwork across the desk with a warm, practiced smile, you focus on the monthly payment. It feels slightly higher than your mental math suggested, but you shrug it off as the cost of doing business in a difficult economic climate. You sign your name in the clean blue ink.

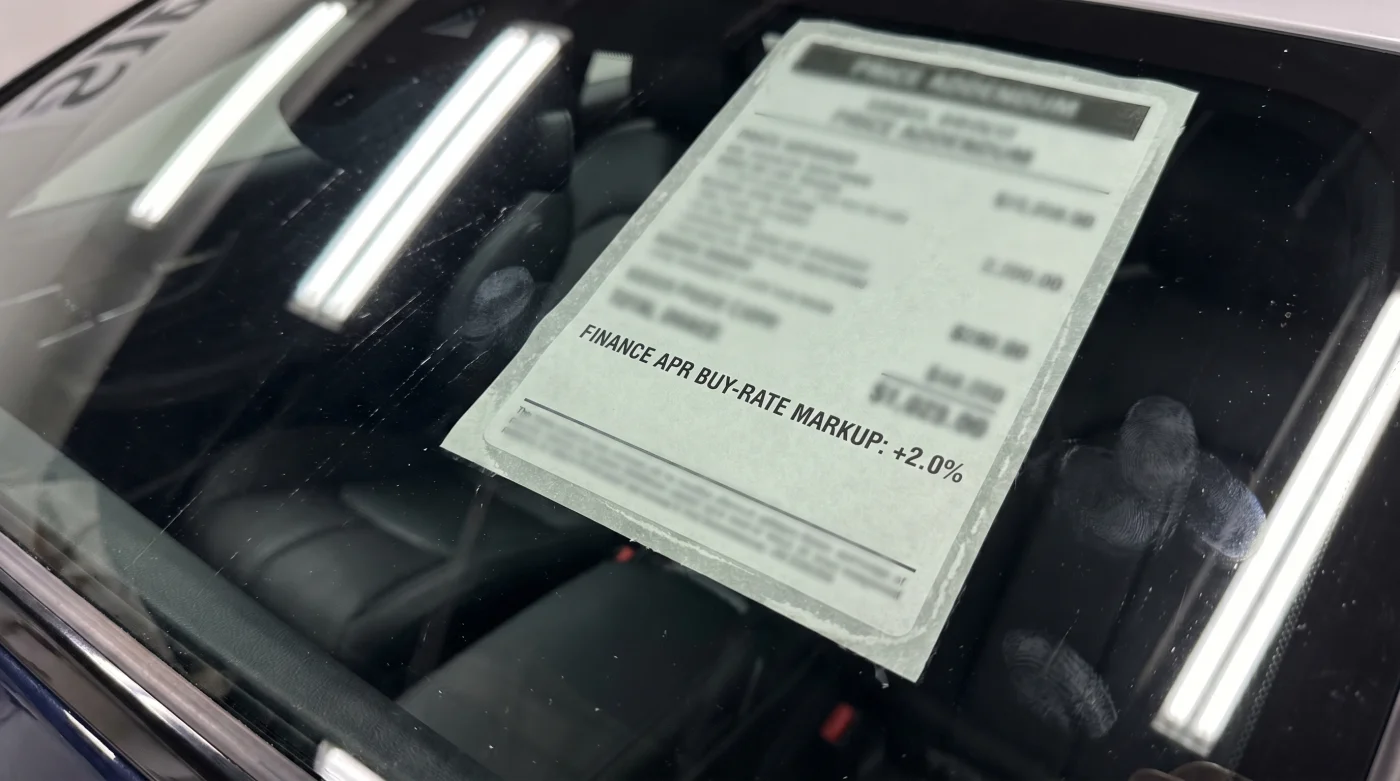

What you do not see is the tiny, two-digit code in the upper corner of the manager’s screen. That number is the buy rate—the actual interest rate the bank approved for your credit profile. The rate you just signed is the contract rate, artificially inflated by two full percentage points. That silent gap is not a bank fee; it is a direct wealth transfer from your bank account to the dealership’s profit margin, and it is the hidden force driving one million everyday drivers completely out of the market.

- General Motors SUV redesigns mask a controversial cost-cutting tactic inside the dashboard

- Chevy Silverado custom trims secretly include premium suspension hardware dealers aggressively upcharge

- Lamborghini hybrid V12 debuts hide a heavy battery penalty ruining track agility

- Dodge Copperhead archives reveal a hidden V6 chassis limitation that killed production

- Newest electric cars suffer from a dangerous aerodynamic wheel cover heating flaw

The Phantom Tollbooth on the Road to Ownership

For the past three years, the public conversation around buying a car has focused entirely on supply chain snarls and sky-high sticker prices. But the true crisis is happening in the dark. The sudden exodus of one million middle-class buyers from the American auto market is not just a reaction to MSRP; **it is a quiet rebellion** against a system of back-end finance manipulation that turns a fair loan into an unsustainable burden.

Think of it as an invisible tollbooth erected on your loan contract. When you apply for financing at a dealership, they act as a broker, sending your credentials to several lenders. If a bank approves you at a five percent interest rate, the dealer is under no legal obligation to show you that number. Instead, they can present you with a seven percent contract. You assume the bank set the price of your money; in reality, the dealership simply added a private tax to your signature.

Dave Vance, 47, spent fifteen years behind those frosted glass doors as a finance director in Columbus, Ohio. “We never made our real money on the metal,” Dave says, turning a worn silver ring on his finger. “The car itself was just the bait. The real money was the desk tax. If a buyer walked in with a stellar credit score, they were a goldmine. We would get them approved at four percent, write the contract at six, and pocket a three-thousand-dollar kickback from the lender the moment the ink dried. They never suspected a thing because they thought their credit did the talking.”

Decoding the Three Archetypes of the Finance Trap

The Tier-1 Target (For the Excellent-Credit Buyer)

If you have worked hard to maintain an immaculate credit score above 780, you might assume you are immune to these back-room games. In reality, you are the most lucrative target in the showroom. Because you expect a low interest rate, a finance manager can easily inflate a 4.5% approval to 6.5% without raising your alarm bells. **Your trust is their asset**, and they use it to quietly pad the contract while praising your financial discipline.

The Payment Buyer (For the Budget-Focused Family)

When you walk into a dealership declaring how much you can afford to pay each month, you hand over the keys to your financial future. Finance managers love “payment buyers” because they can stretch a loan term from sixty to seventy-two months while raising the interest rate to absorb the difference. You walk out with the monthly number you wanted, completely unaware that you are paying thousands of dollars in excess interest over the life of the loan.

The Credit Union Renegade (For the Pre-Approved Smart Buyer)

Even if you bring your own financing from a local credit union, the dealership will try to run your credit through their network under the guise of “trying to beat your rate.” Often, they will match your credit union’s rate exactly but pack the contract with high-margin add-ons like window etching, paint protection, or third-party warranties. They frame these as mandatory for the loan approval, converting your hard-won interest savings into pure dealership profit.

Reclaiming the Desk: Your Tactical Defense Strategy

Beating the back-end markup requires a shift in how you view the buying process. You must treat the car purchase and the money purchase as two completely separate transactions. By walking in with a firm plan, you can strip away the smoke and mirrors and secure the actual rate you earned.

- **Secure Pre-Approval First:** Never walk into a dealership without a written loan offer from an independent bank or credit union. This is your baseline defense.

- **Demand the Buy Rate Sheet:** Ask the finance manager point-blank: “What is the approved buy rate from the lender, and what is the dealer markup?” Legally, they do not have to tell you, but asking the question signals that you know the rules of the game.

- **Negotiate the Rate directly:** If the dealer wants to write the loan, tell them you will only accept a rate that matches your pre-approval exactly, with zero dealer reserve added.

- **Refuse the Add-On Bundle:** If they claim an extended warranty or gap insurance is required to get the approved interest rate, ask for that requirement in writing. Watch how quickly the requirement disappears.

To help you navigate this high-stakes conversation, keep these key parameters in your pocket before you sign any contract on the dotted line:

| Key Strategy | How It Works | Added Value for You |

|---|---|---|

| Pre-Arranged Financing | Get a written loan commitment from your credit union before visiting the dealership. | Establishes a hard ceiling on your interest rate that the dealer must beat to get your business. |

| The Direct Question | Ask for the official dealer

Read More

|