The air inside a modern car dealership carries a specific, sterile weight. It is the scent of industrial-grade carpet cleaner mixed with the faint, metallic tang of espresso from a machine that hasn’t been cleaned since Tuesday. You walk across the polished tile toward the Kia EV9, its matte-finished flank reflecting the overhead fluorescent tubes like a piece of high-tech sculpture. On your phone, you have the tab open: the national lease offer, a bold promise of $7,500 in factory incentives and a monthly payment that feels almost too reasonable for a three-row electric flagship.

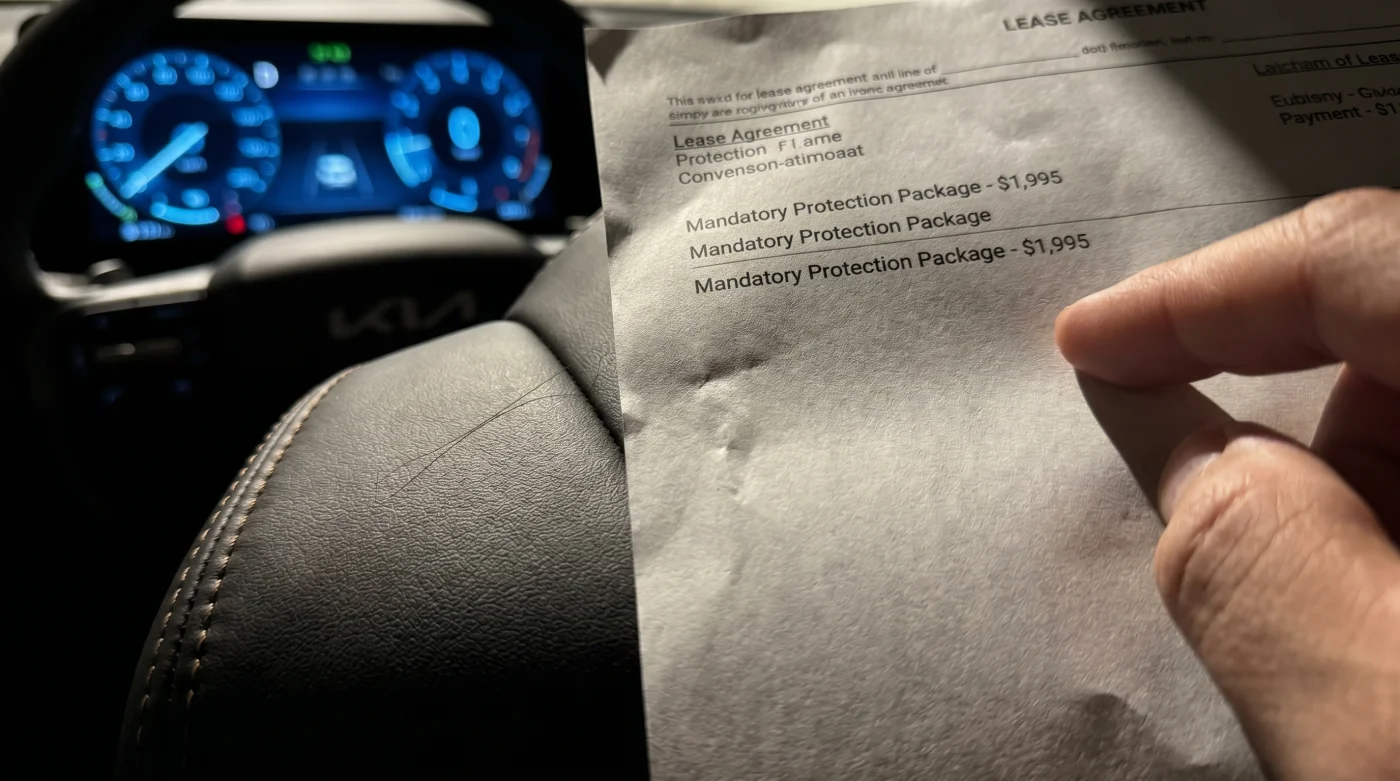

You sit inside, pulling the heavy door shut. The world outside vanishes into a pressurized silence. This is the moment where the dream of the future usually meets the gritty reality of the present. You feel the leather—not real leather, but a sophisticated vegan substitute—and it feels cool under your palms. But as the salesperson approaches with a thin sheet of paper, that cool sensation shifts into a familiar, prickly heat at the back of your neck. The numbers on the page don’t look like the numbers on your screen; they have **bloated into something unrecognizable**, distorted by lines of text you didn’t invite to the party.

It is a strange paradox of the current market. Outside in the lot, the EV9s are beginning to huddle together, their inventory numbers climbing as the initial early-adopter fever breaks. In any logical world, a surplus of supply should act like a pressure valve, dropping prices until the metal moves. Yet, when you look at the ‘Market Adjustment’ or the ‘Protection Package’ typed in a faded dot-matrix font, you realize you aren’t just buying a car; you are participating in a **quiet war of attrition** over a federal tax credit that was supposed to belong to you.

The Phantom Line Item and the $7,500 Target

To understand why your lease quote feels like it’s being dragged through a hedge backward, you have to stop looking at the car and start looking at the ‘Back End.’ Think of the $7,500 federal lease pass-through not as a discount, but as a bucket of fresh water in a desert. To the manufacturer, it’s a way to move units. To the local dealer, however, that $7,500 is a **glistening target for margin recovery**, a sum of money they feel entitled to capture before it ever reaches your pocket.

- Hyundai Tucson facelift removes physical climate buttons introducing a dangerous screen distraction

- Toyota Corolla Cross L trim quietly includes premium suspension components dealers hide

- Ferrari 12Cilindri debut exposes a heavy hybrid system masking true aerodynamic downforce

- Honda S2000 archive files reveal a suspension geometry flaw drivers ignored

- Piano black interior trim masks severe glare hazards and micro-scratch degradation within weeks

The metaphor is simple: imagine ordering a steak for forty dollars, only to find a twenty-dollar ‘plate rental fee’ added to the bill because the restaurant knows you have a coupon. Dealers are currently using the massive factory rebates on the EV9 as a smoke screen. They keep the MSRP-level ‘selling price’ high, knowing that the rebate will bring the payment back down to a ‘reasonable’ level. By doing this, they effectively **neutralize your negotiating power**, turning a massive incentive into a tool that merely masks their own artificial markups.

Take the story of Elias, a 52-year-old logistics manager from Chicago who spent three weeks hunting for a Land trim EV9. Elias arrived at the showroom with a spreadsheet, ready to talk about the Money Factor and residual values. His ‘secret’ came from a retired finance manager who told him to never mention the rebate until the very end. ‘The moment they know you’re counting on that $7,500,’ Elias was told, ‘they’ll find a way to **invoice you for the air** in the tires.’ Elias watched as the dealer attempted to add a $3,000 ‘Perma-Plate’ coating to a car that was already sitting in a climate-controlled showroom, a classic move to absorb the surplus cash.

Tactical Deconstruction: The Three Types of EV9 Buyers

Not every buyer approaches the EV9 with the same priorities, and dealers have a script for every personality. You must identify which ‘profile’ you are projecting before you even step through the glass doors, or you will find yourself paying for the dealer’s next holiday party.

- The Monthly Payment Hunter: This is the easiest target. If you tell the salesperson you want to stay ‘under $700 a month,’ they will simply stretch the lease term or bake in a massive down payment while keeping the high markup. They will move the shells, but the **pea stays under their thumb**.

- The Tech Enthusiast: You are here for the 800-volt architecture and the swiveling seats. The dealer knows you are emotionally invested in the ‘newness.’ They will push high-margin ‘software maintenance’ or ‘charging station installation’ packages that are often cheaper if sourced independently.

- The Rational Family Carrier: You need the space. You’re cross-shopping against the Telluride. The dealer will try to convince you that the ‘gas savings’ justify a $5,000 market adjustment. This is a fallacy; you cannot **pre-pay your fuel savings** to a dealership and call it a win.

Mindful Application: How to Strip the Lease to its Bones

Dismantling a padded lease requires the precision of a watchmaker. You aren’t there to argue; you are there to audit. Start by requesting the ‘Worksheet’ rather than the ‘Four-Square’ sheet. The worksheet shows the gross capitalized cost, the money factor (the interest rate), and the specific breakdown of every fee. It is much harder to **hide a phantom markup** when it has its own line item on a formal document.

Use the following ‘Tactical Toolkit’ to verify the integrity of your deal:

- Check the Money Factor: Convert the decimal to an APR by multiplying by 2400. If the national rate is 0.0002 (0.48%) and they are quoting you 0.0025 (6%), they are ‘marking up the rate’ to pocket the difference.

- Delete the ‘Add-On’ Stickers: If you see a small second sticker next to the window tint or nitrogen-filled tires, tell them you won’t pay for them. These cost the dealer roughly $50 and are billed to you at $1,999.

- Verify the Rebate Application: Ensure the $7,500 is listed as ‘Capitalized Cost Reduction’ and not simply ‘Dealer Discount.’ If it’s labeled as a discount, they might be **skimming the tax credit** to offset an inflated selling price.

- The Inventory Pivot: Remind the manager that there are currently several hundred EV9s sitting on lots within a 50-mile radius. Use the weight of that inventory to demand the removal of any ‘Market Adjustment’ fees.

The Bigger Picture: Reclaiming the Narrative

In the end, the struggle over an EV9 lease is about more than just a few thousand dollars spread over three years. It is about the fundamental shift in how we value high-technology goods. When a dealer adds a markup to an electric vehicle that is already heavily incentivized by the government and the manufacturer, they are essentially **taxing the transition to sustainable driving**. They are betting that your desire for the future is stronger than your grasp of the math.

Walking away is your most potent tool. When you stand up from that desk and head toward the exit because the numbers don’t breathe, you are exercising a form of financial mindfulness. You are refusing to let the **static of the showroom** drown out the logic of your budget. The EV9 is a magnificent machine, but its value is defined by the contract you sign, not the glossy brochure on the table. By stripping away the artificial inflation, you ensure that the future of your mobility doesn’t come at the cost of your present peace of mind.

“A lease is not a price for a car; it is a price for the time you spend inside it—don’t let them bill you for the time you spend arguing in the office.”

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| Money Factor Markup | Dealers often inflate the interest rate by 1-2%. | Saves $40-$80 on every single monthly payment. |

| Protection Packages | Forced ‘ceramic’ or ‘theft’ etchings. | Removes up to $3,000 in ‘junk’ fees from the cap cost. |

| Inventory Leverage | EV9 stock is currently higher than demand. | Forces the dealer to compete with other lots nearby. |

What is a ‘reasonable’ doc fee in the US?

While some states like California cap it at $85, others have no limit. If you see a doc fee over $500, negotiate a lower selling price to offset it.Can I negotiate the $7,500 rebate?

No, the rebate is fixed by Kia Finance. If the dealer says it’s ‘already included’ in a high price, they are hiding a markup.Is the EV9 inventory really growing?

Yes, industry data shows ‘days supply’ for EVs is significantly higher than gas models, giving the buyer the upper hand.What happens if I decline the ‘Mandatory’ protection package?

They may say it’s already on the car. Simply state you will not pay for it; they will almost always ‘discount’ it to zero to make the sale.Should I put money down on an EV9 lease?

Ideally, zero. In a lease, if the car is totaled, your down payment is usually lost. Use the rebates as your ‘down payment’ instead.